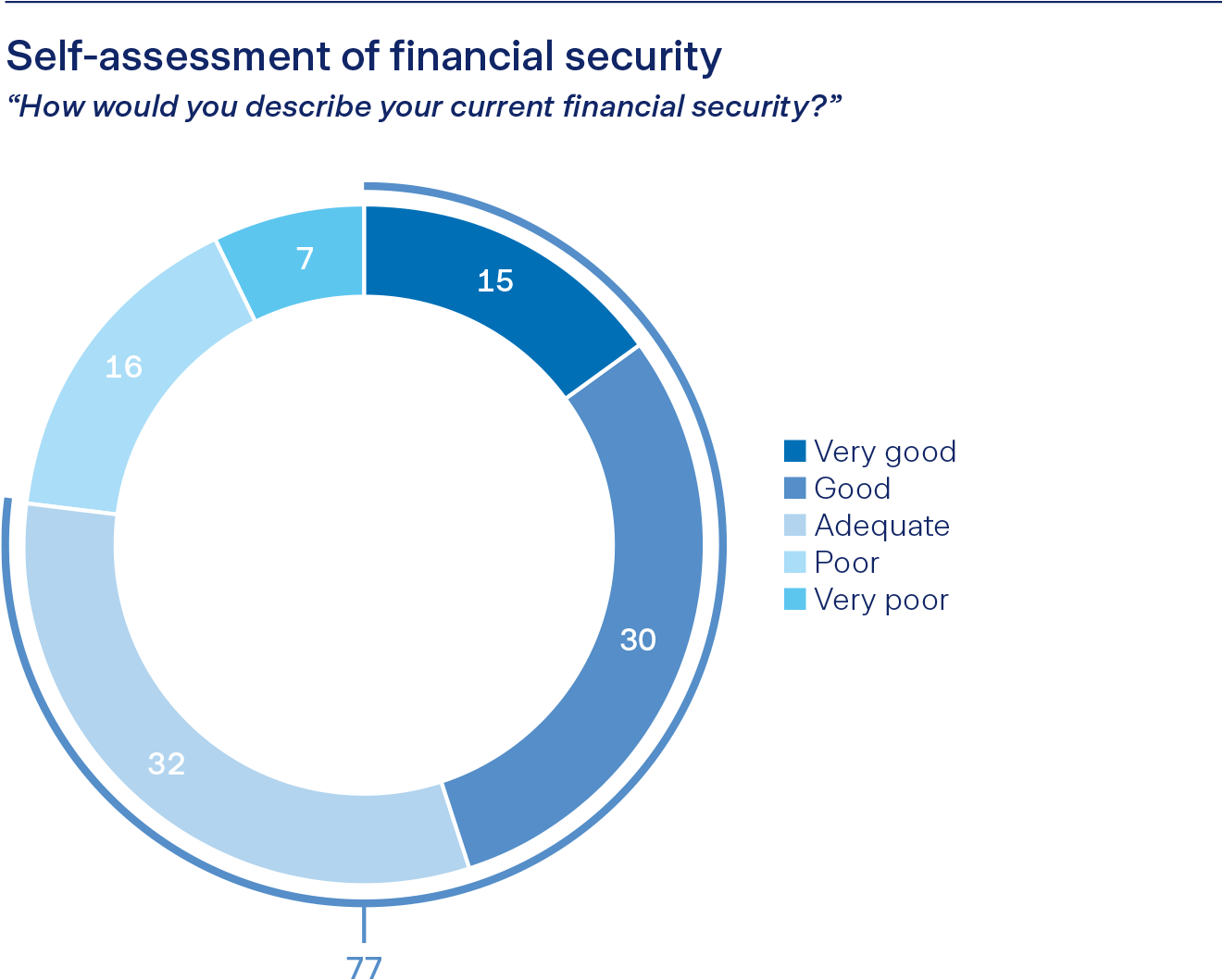

How Switzerland is doing financially

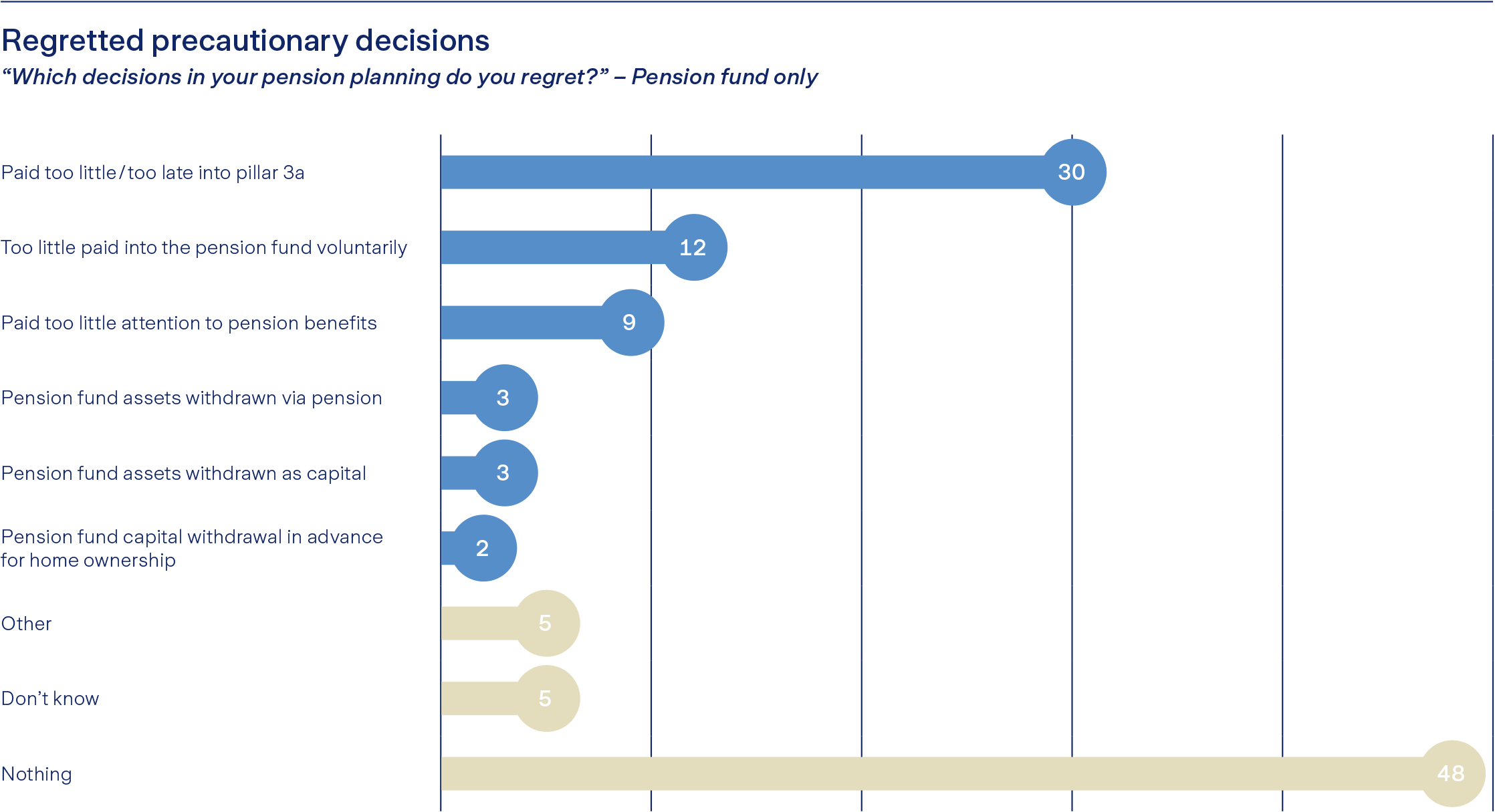

Most people in Switzerland are doing well financially. Nevertheless, one-third of the population have financial worries that affect their personal well-being. The latest "Fairplay" study on the topic of finance and security also shows which pension decisions people regret in old age and why money makes people happy after all.