Switzerland is aging: Why demography concerns us all

Demographic change has an impact on all areas of life. That's why it's important to be in the know.

Switzerland is getting older: Life expectancy is increasing and, at the same time, fewer and fewer children are being born. The average age of the population is rising, and the proportion of older people is increasing.

The changes are a challenge for society as a whole – and for each and every individual. It is therefore important to engage with this topic and act with foresight.

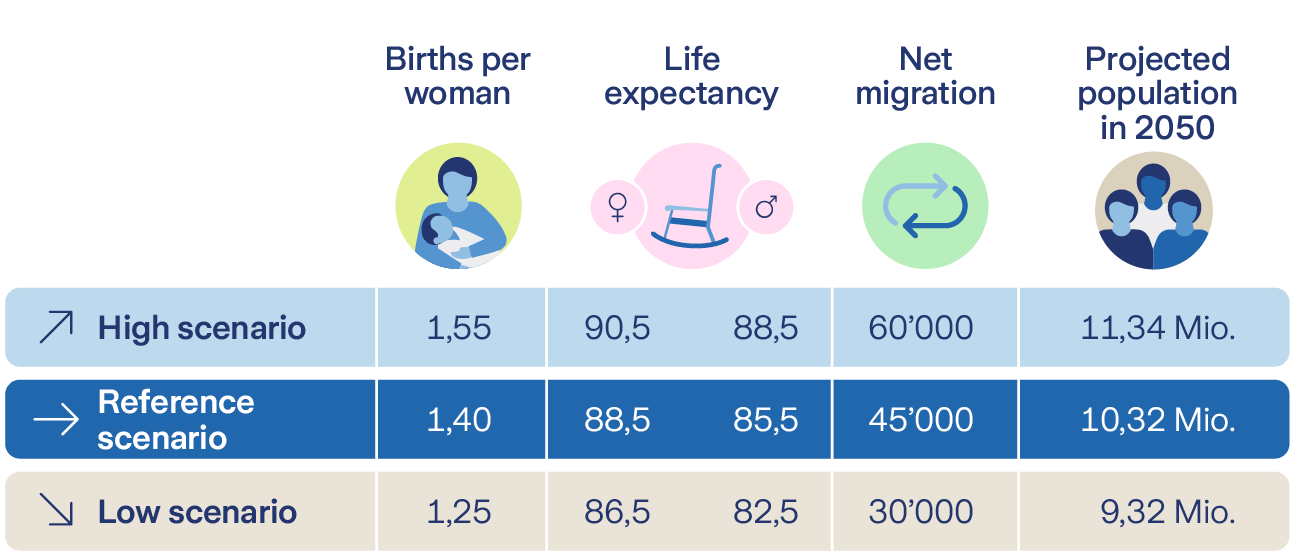

According to the latest population growth scenarios from the Federal Statistical Office for 2025, there will probably be – without any far-reaching political intervention – between 9.32 and 11.34 million people in Switzerland by 2050, with the most likely scenario assuming 10.32 million people. The scenarios depend primarily on three factors: birth rates, life expectancy and immigration.

More pensioners in relation to the working population

At the same time, the aging quotient will increase. This describes the ratio of people of retirement age (65+) to people of working age (20 to 64). From 2025 to 2050, the ratio is expected to shift from 33 to 100 to 43.3 to 100. This means: Today, there are 3 working people for every 1 pensioner; by the middle of the century, the ratio will probably be close to 1 to 2. The number of very old people (80+) will also rise sharply. In 2025, 6 percent of the population was over 80 years old. By 2050, this figure is likely to be 9.7 percent, i.e. almost one in ten people.

Demographic change in Switzerland is influenced by three key factors:

Birth rate:

Fewer children have been born for decades, and the birth rate is currently at a historic low: While the number of children per woman was 2.7 in 1964, it is now only 1.29. However, a constant population with a balanced age structure would require 2.1 children per woman. Without immigration by predominantly young people, the aging effect would be even more pronounced.

Life expectancy:

Thanks to medical advances and better living conditions, life expectancy in Switzerland is rising steadily, and after a mini dip due to coronavirus in 2020, the trend is continuing. Currently (2024), women will live to 85.9 years of age on average and men to 82.4. The difference between the sexes is therefore 3.5 years and getting smaller: In 1990 it was still almost 7 years.

Once you have reached retirement age (65), your life expectancy is even higher: Currently, a man can expect to live for 20.4 years, a woman for 23 years. This figure has also risen steadily. So more and more people are reaching an advanced age, and the proportion of elderly people in the population is growing. At the same time, the money saved up until retirement must now last much longer than in the past.

Migration:

Immigration plays an important role in population development: If more people immigrate than emigrate, the population increases. Because migrants are usually young, they have a positive effect on the population structure and bring down the average age. In all scenarios, the Federal Statistical Office assumes that fewer people will come to Switzerland from the 2030s onwards, as neighboring European countries are also facing similar demographic challenges: They will have fewer young people, and they will be needed in their own countries.

Demographic change has far-reaching effects on key areas of our lives and society:

Social security and pension system

Rising life expectancy and the growing proportion of older people pose major challenges for the OASI pay-as-you-go system (state retirement provision). This is because fewer and fewer working people have to finance more and more pensioners who are drawing benefits for longer and longer. This is upsetting the balance in the intergenerational contract. Without adjustments, there is a risk of higher contributions or lower pensions. The situation is less dramatic in occupational retirement provision, or BVG, and in private retirement provision. This is because everyone saves for themselves there.

Healthcare

With more very old people over the age of 80, the need for medical care and nursing services is increasing. This is because many people are increasingly dependent on help in their final years. It is a major social task to ensure this support and thus enable the highest possible level of autonomy and quality of life even in old age. Accordingly, more specialists are needed, as well as innovative care concepts. Nevertheless, these solutions must remain affordable.

Labor market

The declining proportion of young workers in the population could lead to a shortage of skilled employees. An aging society may also be less able to fully exploit the potential of artificial intelligence, for example. On the other hand, demographic trends can create opportunities, for example for older employees who want to stay in work for longer. The importance of further training and flexible working models also increases.

Infrastructure

If there are more older people and fewer younger people, this also has an impact for infrastructure: There is more need for accessible homes, new ideas for intergenerational cohabitation and neighborhoods in which older people can remain mobile and participate in social life.

Prosperity

An aging society may threaten Switzerland's prosperity. This risk can be mitigated with appropriate solutions to the demographic challenges. It is possible that artificial intelligence will help to make up for the shortage of skilled workers and ensure productivity and success even with fewer employees.

Conclusion

Demographic change harbors risks for financial stability and provision – but it also opens up opportunities for innovation, new life models and greater intergenerational solidarity.

Changes in the age structure and the demographic shift have a direct impact on everyone's retirement provision planning. Anyone who is currently in work must assume that state and company benefits will become less and less capable of allowing them to maintain their current standard of living. This makes private retirement provision all the more important as a necessary supplement.

Identify and close pension gaps

With increasing life expectancy, the time spent in retirement is getting longer, which means that money has to last longer. At the same time, there is much to suggest that the state pension level at least will fall in the coming decades. More expenditure, less income: The result is pension gaps. It is therefore more important than ever to analyze your own pension situation at an early stage and actively improve it.

In view of the demographic shift, private retirement provision is an indispensable building block for financial security in old age. Those who act today will remain independent in future.

Have your personal pension situation analyzed regularly: Check the current status, close any gaps and take demographic trends into account when planning for the future.

At Zurich, we advise people on retirement provision every day and experience first-hand how much demographic change concerns many people. At the same time, in countless consultations we discover how people are successfully setting the course for financial freedom in their old age with targeted decisions.

Practical tip from our consultants: The earlier, the better

Anyone who only starts thinking about retirement provision "in the middle of life" is missing out on important opportunities. It is worth starting to save at a young age to benefit from the compound interest effect to the maximum. In this way, a significantly higher result can be achieved with the same input.

Checklist: Important questions for retirement provision

We support you in finding answers to these questions – and in drawing the right conclusions.

At Zurich, we provide you with comprehensive advice on all retirement provision topics. Pension or financial planning is also possible. We look forward to hearing from you!

With professional support from

As a technical expert at Zurich, he contributes his expertise in retirement provision and investments.