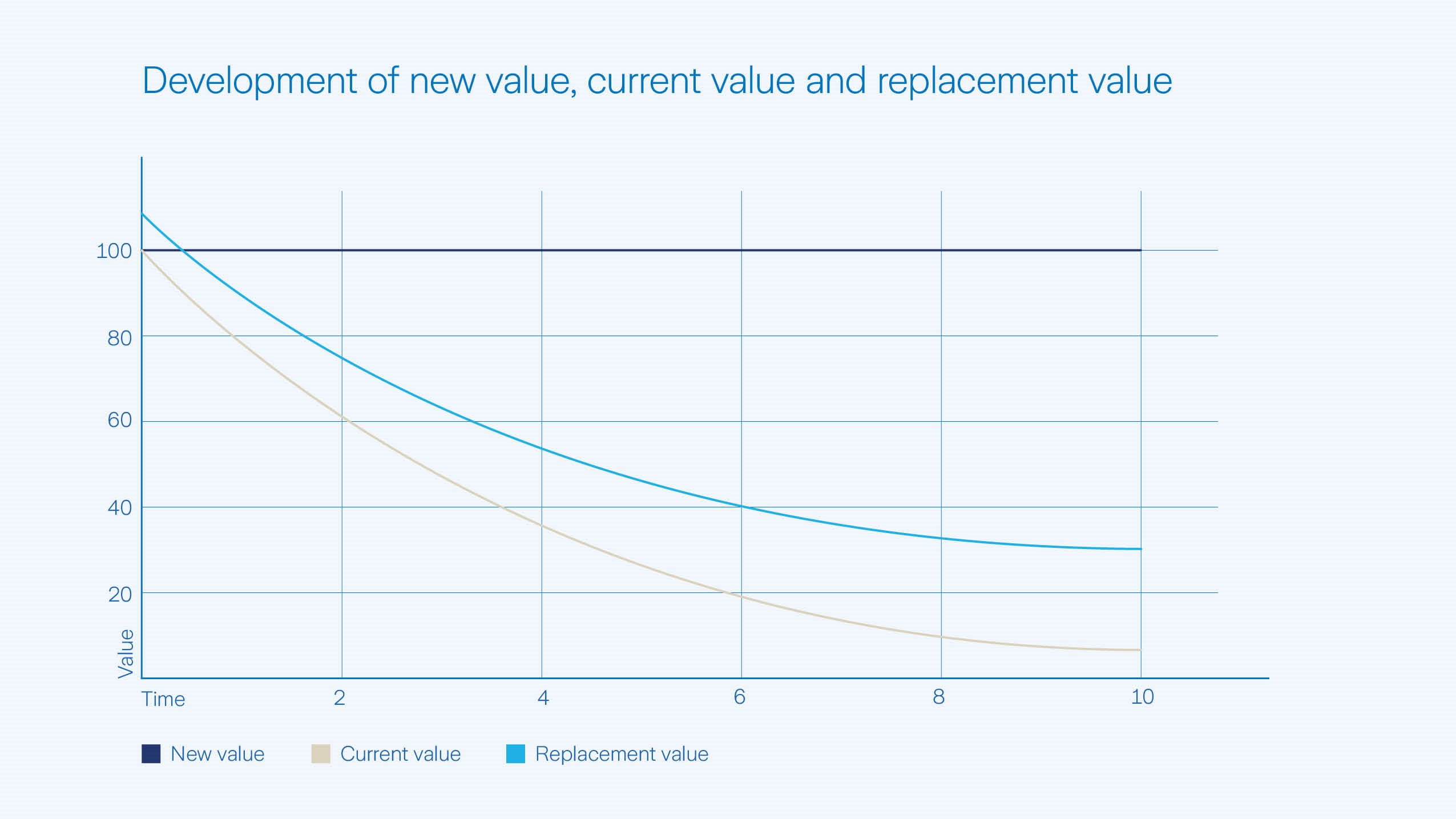

The value you receive from Zurich in the event of a loss depends on the insurance cover you choose. If an item or your building is insured at replacement value, the replacement value will be reimbursed in the event of a loss. With cash value insurance, on the other hand, you receive the cash value of the damaged or lost property. You should therefore carefully check which cover makes sense for your situation when you take out the policy.

Household contents insurance

As a rule, replacement value cover applies for household contents insurance.

This means: if your household contents are damaged or stolen, the insurance will reimburse the amount you need to buy new items of the same value.

Household contents include, for example:

- Furnishings

- Clothes

- Electronic devices

- Household appliances

It is important that the sum insured is set sufficiently high. Only then can the claim be fully compensated.

Exception for caravans and mobile homes. If caravans or mobile homes are included in the household insurance, compensation is paid at cash value.

More about Household contents insurance.

Buildings Insurance

Buildings are usually insured at replacement value.

In the event of a loss, the insurance covers the costs of rebuilding or restoring an equivalent building at the current construction value.

Certain technical building systems, such as photovoltaic systems, can also be insured against internal and external damage. If such a system is damaged, the compensation in the event of a loss is based on the age of the system.

More about Buildings Insurance.

Motor vehicle insurance

The types of compensation in motor vehicle insurance determine how much is compensated in the event of a loss:

- Replacement value compensation: in the event of a total loss, the amount paid out is the amount that the vehicle would have had in brand-new condition. Replacement value compensation is often only valid for a limited period after initial registration (12 or 24 months).

- Purchase price protection/purchase price guarantee: is available as additional cover for new or used cars. The maximum compensation is the purchase price paid, for 5 years from the date of purchase.

- Cash value plus supplements: this is the most common type of compensation for vehicles up to the 7th year of operation. The cash value plus supplements is defined in a table. Compensation in the event of a total loss is calculated as a percentage of the original new value of the vehicle and is based on the respective year of operation. Thanks to the cash value plus supplements, the compensation is significantly higher than the pure cash value of the vehicle.

- Cash value or replacement value: these types of compensation apply to older vehicles from the 7thyear of operation.

More about Car insurance.