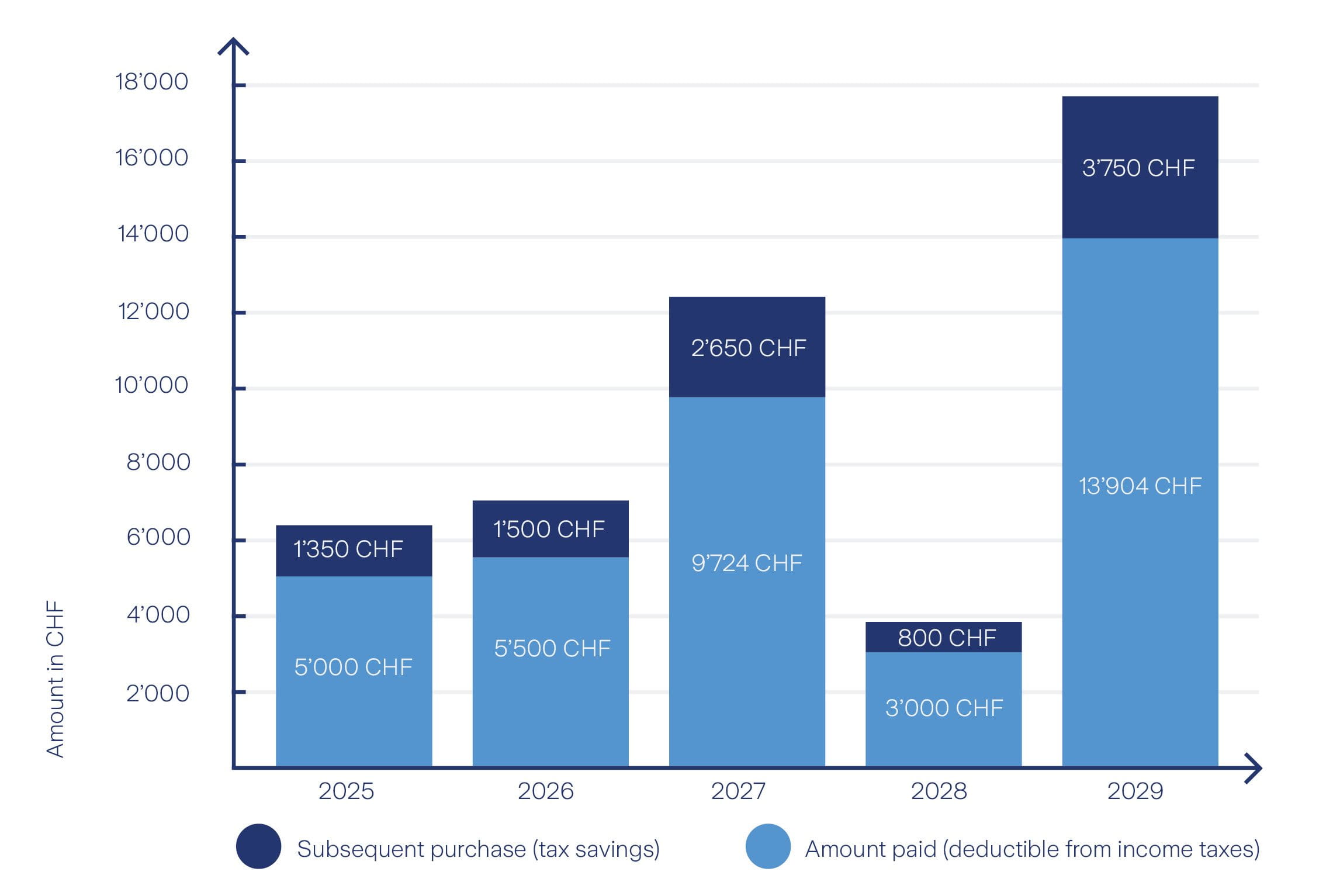

Top-up payments into pillar 3a: How to close retirement provision gaps

From 2026, employed persons in Switzerland will be able to make up for missed payments into pillar 3a for the first time – and thus not only close pension gaps, but also make the most of their tax potential. This is particularly attractive for anyone who was unable to make full contributions in the past for financial reasons and would now like to improve their retirement provision in a targeted manner.